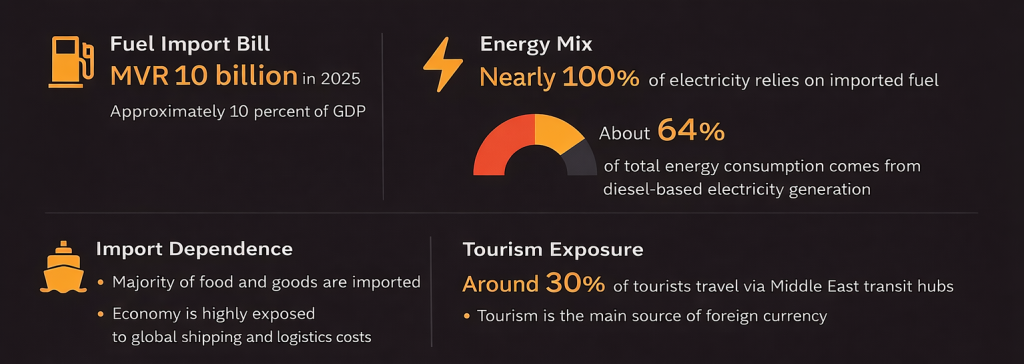

MVR 10 billion. That is how much the Maldives spent on fuel imports in 2025, according to the finance minister, an amount equivalent to roughly 10 percent of national output. In a small, import-dependent economy, that is not just a line item in the budget. It is a structural exposure. The ongoing Middle East conflict has made that exposure visible, as disruptions to global energy markets begin to feed directly into domestic costs, fiscal pressure, and economic uncertainty.

The global shock has been both immediate and unusually severe. The disruption of the Strait of Hormuz, a chokepoint that typically carries around 20 percent of global oil supply, has sharply reduced maritime traffic and pushed energy prices upward. In the early phase of the conflict, Brent crude rose above $100 per barrel. At the same time, global shipping has been forced into detours of up to 4,000 nautical miles, adding as much as two weeks to transit times and driving up freight costs. Air transport has also been affected, with over 5,000 flights cancelled within the first 48 hours of escalation, disrupting key transit hubs that handle roughly 14 percent of global international traffic.

For the Maldives, these global shifts are not abstract. They are transmitted through three channels that define the country’s economic structure: energy imports, trade dependence, and tourism flows. Electricity generation relies almost entirely on diesel, meaning higher global oil prices translate directly into higher domestic costs. The country imports most of its goods, so rising shipping and insurance costs feed into higher prices at the consumer level. Tourism, which provides the bulk of foreign currency earnings, depends heavily on long-haul travel routes that have now become more expensive and less reliable.

This combination creates a feedback loop. As fuel prices rise, the import bill increases, placing pressure on foreign exchange reserves. At the same time, disruptions to aviation reduce tourist arrivals, weakening the inflow of dollars needed to finance those imports. The result is a widening gap between what the country earns and what it must spend, a dynamic that becomes more difficult to manage as global conditions remain unstable.

The cost of this dependence is already visible. Fuel import bills rise not just because of higher prices, but because there are few alternatives. Electricity must still be generated, transport must still function, and resorts must still operate. To prevent these costs from being passed fully onto households and businesses, the government absorbs part of the increase through subsidies. This creates a second layer of pressure, as public spending rises at the same time that revenues face uncertainty.

These dynamics are not theoretical. In previous years, fuel subsidies have reached levels that strain the budget, and the current environment risks pushing them further. The practical effect is felt across the economy. Electricity tariffs are kept artificially low in some areas, while businesses in others face higher costs. Transport becomes more expensive, raising the price of goods. For households, this translates into a gradual increase in the cost of living, even when headline inflation appears contained.

Against this backdrop, the Maldives has already begun a transition towards renewable energy, though at a measured pace. Solar power has expanded in recent years, with installed capacity increasing and projects spreading across inhabited islands and resort properties. Programmes supported by international partners have helped reduce the cost of solar electricity, making it increasingly competitive with diesel generation.

The scale of this progress is meaningful but still limited. Renewable energy accounts for a growing share of the electricity mix, yet diesel remains dominant. The country has set targets to increase renewable penetration significantly over the coming years, supported by investments in solar installations and battery storage. These efforts reflect a recognition that energy dependence is not sustainable in the long term.

The pace of transition, however, is shaped by constraints that are specific to the Maldives. Financing remains a central challenge. Renewable infrastructure requires upfront capital, while the benefits are realised over time. For a country managing high debt levels and limited fiscal space, mobilising this investment is not straightforward. Geography presents another constraint. With islands spread across a wide area, there is no single national grid. Each island effectively requires its own system, increasing costs and complexity.

There are also technical and regulatory challenges. Integrating solar power into small, isolated grids requires storage solutions to manage variability. Battery systems, while becoming more affordable, still add to the overall cost of projects. Environmental considerations, particularly in marine ecosystems, shape how and where renewable infrastructure can be deployed. These factors slow down implementation, even when the economic case is clear.

That economic case has become stronger as global energy volatility increases. Unlike diesel, which must be imported continuously and paid for in foreign currency, solar energy relies on upfront investment but has minimal operating costs. Once installed, it reduces exposure to global price fluctuations. In practical terms, this means fewer dollars leaving the economy and greater predictability in energy costs.

Over time, the difference is significant. Lower electricity generation costs reduce pressure on public finances and improve the competitiveness of businesses, particularly in tourism. More importantly, they reduce the economy’s vulnerability to external shocks. In a world where energy markets can be disrupted by geopolitical events, this stability has value beyond simple cost savings.

The current conflict serves as a stress test for the Maldivian economic model. It highlights how quickly external events can affect domestic conditions, not through dramatic policy changes but through the basic mechanics of trade and energy. It also reveals the limits of short-term responses. Subsidies and supply diversification can mitigate immediate impacts, but they do not change the underlying structure.

What is being tested is not just resilience, but adaptability. The Maldives has long operated within a system where imported fuel is a given, and where global stability is assumed. The events of 2026 challenge that assumption. They suggest that volatility in energy markets may not be an exception, but a recurring feature of the global economy.

The trajectory depends on how long the current disruption lasts. A short-lived conflict would ease pressure on oil prices and restore some stability to transport and tourism. A prolonged period of instability would embed higher costs and uncertainty, making the existing model more difficult to sustain. In either case, the direction of travel is clear. The risks associated with fossil fuel dependence are no longer hypothetical.

The broader lesson is that energy policy is economic policy. For the Maldives, the transition to renewable energy is not simply about meeting climate commitments or aligning with global trends. It is about reducing exposure to risks that originate far beyond its borders. The current crisis makes that connection visible. It shows that the cost of dependence is not fixed, but variable, and that it can rise sharply when global conditions shift.

What remains is a question of timing. The longer the transition takes, the longer the economy remains exposed to these shocks. The events unfolding now are unlikely to be the last of their kind. In that sense, the issue is not just how the Maldives responds to this crisis, but how it prepares for the next one.